After hyping Bitcoin for so many years, I’ve written quite a few articles, but on careful reflection, I still haven’t written a popular explanation of Bitcoin’s basic principles. Although you can find a ton of them with a casual search online, I haven’t found one that really suits my taste. During a spell of battling Shanghai’s heat, I had a sudden urge to write one myself and see how it goes.

(This article is obviously not very timely; what’s hot lately is the Bitcoin fork crisis. I posted two Weibo updates about this issue recently, and they’re appended at the end.)

I hope to explain Bitcoin’s basic principles in as popular and accessible a way as possible, without getting too much into questions such as whether Bitcoin is worth anything or whether it is a scam. I’ve already written about these defensive arguments elsewhere.

Many people’s confusion about “Bitcoin” has to do with the ambiguity of the concept itself. “Bitcoin” can refer to a unit of currency, it can refer to an open-source software program, and it can also refer to a set of network protocols or the corresponding network system, and so on.

By comparison, “renminbi” doesn’t have this kind of ambiguity. When we ordinarily speak of renminbi, we mean the unit of currency—that is, “money.” Of course, behind “money” there is also a whole series of things, such as containers for money (wallets, bank cards), exchange and settlement institutions (banks), issuing and regulatory institutions (the central bank, printing plants), and so on.

The concept “Bitcoin” loosely covers an entire system of things ranging from money and wallets to banks and printing plants. No wonder it seems so elusive. If we unpack these links one by one, then Bitcoin will not be harder to understand than renminbi.

1. Unit of measure: Bitcoin vs. yuan, jiao, fen

If we are only talking about the currency unit, there is actually nothing hard to understand. It’s nothing more than a measuring symbol. For example, today 1 dollar can be exchanged for 6.8 renminbi, 1 ounce of gold can be exchanged for 1,240 dollars, one bottle of Maotai costs around 2,000 renminbi, one lot of Maotai stock is 473 renminbi… Similarly, 1 bitcoin can be exchanged for 19,000 renminbi, and there is no essential difference from the examples above.

In terms of “units of measure,” “uniform divisibility” is a common feature of the things mentioned above—Bitcoin, gold, renminbi, stocks, and even Maotai liquor. By uniform divisibility, I mean first that it can be split and combined: 2 kilograms of gold can be divided relatively easily into two 1-kilogram pieces of gold, with basically no change in value. 2 yuan can be divided into two 1-yuan notes or coins, again with basically no change in value. Obviously not every commodity is like this. For example, if a 2-carat diamond is cut into two pieces, its value changes; 1+1≠2.

Even when something can be split, there are differences in how difficult the splitting is, how fine a division can be achieved, and how uniform the result is after splitting. For example, converting 10 yuan into two 5-yuan notes can be done by any street vendor, but converting a piece of gold into two pieces of exactly equal weight requires going to a specialized place, and it costs something. On the other hand, the smallest unit into which renminbi can be divided is 1 fen; gold may be cut into arbitrarily small pieces, but that also depends on the level of craftsmanship.

As for uniformity, gold and silver have issues of fineness and purity; two pieces of gold with the same weight may not have exactly the same value. In theory, renminbi is completely equivalent, but different “containers” still vary somewhat. For example, on buses only coins are accepted; ATMs only accept new 100-yuan notes; this shop allows card payment, that shop allows Alipay, and so on. Even when it is all “1 yuan,” what sits in a bank card and what sits in Alipay are not necessarily identical.

Money is, in essence, also a kind of commodity that can be exchanged in the market, but not every commodity is suitable to serve as money. “Uniform divisibility” is a basic characteristic of money. The easier something is to divide, the more uniform and homogeneous it remains after division, and the easier it is to measure, the more suitable it is to become money and be used to measure the value of other commodities.

From this perspective, the digitization of money is undoubtedly the general trend. After all, when it comes to the ability to be uniformly divided, no physical object can compare with abstract numbers. No cutting is needed, no change is needed; you can divide it however you want.

At present, the smallest unit into which Bitcoin can be divided is the “satoshi,” and 1 bitcoin = 100 million satoshis. This precision is certainly more than sufficient right now. As for the future, if needed, it would be easy to upgrade with community consensus, and it is also possible to subdivide further into units smaller than a satoshi.

It is worth noting that here “Bitcoin,” as a unit of measure, is actually seriously confusing, because Bitcoin in fact lacks a classifier; strictly speaking, only “satoshi” counts as a classifier. We know that the classifiers for renminbi are yuan, jiao, and fen; the dollar uses “bucks,” gold and silver use “taels,” Russia uses “rubles,” Britain uses “pounds”… When we calculate prices, we generally say that something sells for “100 yuan,” or “100 yuan renminbi,” rather than saying “100 renminbi.”

The reason this confusion is worth mentioning is that it does in fact cause practical misunderstandings for many beginners—namely, “Bitcoin is too expensive!” When they say this, they often do not mean that the whole Bitcoin network or its total market capitalization is too expensive, but rather that its “unit price” is too expensive: it’s already over ten thousand yuan, so why don’t we just buy altcoins instead? Look, Dogecoin is only 1 fen… But in fact this so-called unit price depends on how the “unit” is defined, and that unit can be defined arbitrarily. For example, if we call Bitcoin’s smallest unit, the satoshi, a “fen,” then 10 satoshis = 1 mao, 10 mao = 1 yuan; then right now “1 yuan Bitcoin” would be only a little over 1 fen in renminbi.

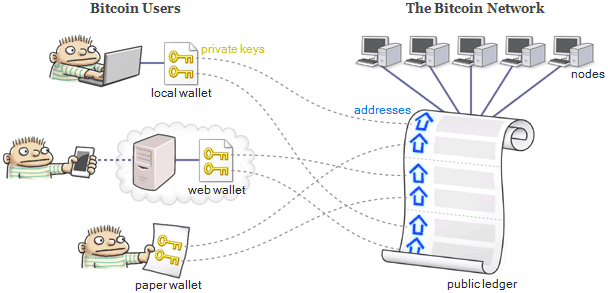

2. The container for money: Bitcoin wallet vs. bank card

The second thing that might be called Bitcoin is the Bitcoin client—for example, if you download the official development team’s client, it may be something like this file: “bitcoin-0.14.2-win64.zip.” Of course, after installation is complete, its name may be “Bitcoin Wallet,” “bitcoin-core,” “bitcoin-qt,” and so on. So what does this software do?

Its function really is like a “wallet”: it mainly provides a container for money. We know that a wallet itself is not money; it merely provides a container for putting money in and taking it out. Such containers can take many forms—plastic, cowhide, and so on—and they affect only the feel, not your wealth. Of course, currency has already been digitized long ago. Apart from physical wallets storing physical currency, most of our money is actually in banks. In that case, bank passbooks, bank cards, and so on can also be said to be the carriers of money.

We may say, “This bank card has a million in it.” What does that mean? It does not mean that if you tear up the card, a bunch of coins will jump out. Rather, it means that in some form there exists a set of records or credentials that allow you, through this bank card, to dispose of the corresponding money.

In fact, when your money is in the bank, to be precise there are not actually any fixed physical objects in the bank that correspond to your deposit. What corresponds to your deposit is nothing more than some numbers. How much money you really have depends on the bank’s records, and the bank card is the credential by which you can modify those records. Through the bank card, you can transfer some of the numbers under your account to someone else—that is “payment.”

Of course, other people can also modify your deposit record, but only by adding, not subtracting. That is to say, others do not need to use your bank card in order to send money to your account; of course, you need to make your bank card number public to them.

So a bank card actually contains two functions: a payment credential and a receiving code. The former is controlled only by you—such as some encryption mechanism inside the bank card, or your online banking password. Only by possessing the payment credential can you use your deposit and pay others. The latter can be made public to others; it is your bank card number, and others can use that number to remit money to you.

Bitcoin, in essence, also has these two functions: payment credential and receiving code. In Bitcoin, these are called the private key and the public key. They are actually just two strings of characters—for example, the private key may look like 5KYZdUEo39z3FPrtuX2QbbwGnNP5zTd7yyr2SC1j299sBCnWjss, and the public key may look like 1YiLinDDwvBLT19CTUsNHdiQhXBENwURb (more precisely, this is the compressed form of the public key, but beginners need not distinguish that finely).

Bitcoin technology is founded on cryptographic principles. We do not need to understand cryptography; we only need to know roughly that cryptography is based on an asymmetry in the difficulty of certain computations and their inverse operations. For example, given several prime numbers A, B, and C, you are asked to multiply them to get D; or conversely, you are first given D and asked to factor it into primes—the latter is the inverse operation of the former, but it is much harder to calculate.

The Bitcoin private key and public key have exactly this relationship: if you know the former, it is easy to compute the latter; but if you know the latter and try to work backward to the former, it is extremely difficult, so difficult that even with all the computing power humans possess now, you could work at it until the end of time and still not get it.

To put it in a more accessible analogy, the private key is like the seal of your company, and the public key is like the name of your company. The person who has the seal of course knows the company name, but knowing the company name does not mean you possess the seal. Conversely, forging a seal is extremely difficult—in the case of Bitcoin, the difficulty is the kind that lasts until the end of time, so there is no need to worry about fake seals. The company name is public; if others want to send you something, knowing the name is enough to find you. But if something is to be issued in the name of your company, only the person who possesses the seal has the authority to do so. Still, exercising that authority does not require sending the seal itself out; you only need to “stamp it,” and what is stamped is a kind of “cross-seam seal.” Each signed document requires a separate stamping, and this cross-seam seal cannot be transferred to another document.

How Bitcoin uses cryptography to achieve this effect is not something an introductory article needs to explain, but in any case it does achieve it. Owning Bitcoin is actually equivalent to owning one or several “accounts,” each of which has a private key and a public key. You possess the private key, and then you make the public key public, especially to people who will remit money to you. Once someone sends money to you, there is money in your account. If you want to use the money in the account, you write a document saying how much money should be sent to whom, then use your private key to stamp this document with a “cross-seam seal,” and then make the document public. When others see the document and confirm that the seal is valid, they recognize that the transaction succeeded, and the money under your account has been remitted.

In short, Bitcoin is really just two strings of characters: the private key is responsible for signing remittances to others, while the public key is responsible for letting others remit money to you. So the question is: I know how to stamp a seal, but I don’t know how to sign with a private key—what should I do? That is precisely the role of the Bitcoin “wallet.” The client software merely provides a container for storing your private key, and then helps you use the private key to sign transactions whenever necessary. Programmers who understand code actually do not need any special software; they can directly issue transactions with a private key. Wallet software simply makes the process more approachable.

So there are countless varieties of Bitcoin wallets, but their common feature must be storing the private key and helping you use the private key. The safest way to store it is simply not to use any wallet software at all: write the private key on paper and lock it in a safe. In that way, even the most brilliant hacker in the world cannot steal your private key. Of course, a thief who physically breaks in and carries off your safe could indeed steal your private key. I won’t go into how to generate such a paper wallet; you can search for keywords like “Bitcoin cold wallet” or “Bitcoin cold storage” to learn more. But from the standpoint of lightness and convenience, online wallets also have their advantages. Of course, online wallets also come in two kinds: real wallets and fake wallets. A so-called real wallet still helps you store and use the private key, and guarantees that only you yourself control the private key; a fake wallet, in fact, does not mean you own the private key at all, but at most that you have a custodial agreement and let the website keep it for you. From the standpoint of security, it is always truly reliable only if you control the private key yourself.

By the way, how do you obtain a private key? You just calculate it yourself according to a certain rule; there is no need for an online environment. With just a few lines of simple code, plus a random-number generator, you can generate a large batch of private keys and the corresponding public keys yourself. Don’t worry that you and someone else will happen to generate the same private key; as long as your random-number generator is working properly, such a “coincidence” would also have to wait until the end of time to happen.

You can amuse yourself by generating a large number of Bitcoin addresses, but having a pile of blank passbooks is of no use. You need to make the generated public keys public. Only after someone has transferred money to you does that public key, and its corresponding private key, become useful. Only after an actual transaction has taken place will your address be recorded in Bitcoin’s public ledger. So if you want to join the holders of Bitcoin, you do not need to find any institution to “open an account”; just find someone to transfer money to you.

3. Initiating a transaction: blockchain vs. bank

A bank card is your credential for making payments, but how much money is actually in your bank card is not decided by the bank card itself; it is decided by the bank. Of course, you may also have a passbook yourself, recording which transactions you have made and what your balance is, but your own ledger does not count. The bank also has a record, and that one is authoritative. If you remember that you have a million and the bank says you have no money at all, then you still won’t be able to spend anything.

So when you swipe a bank card, it ultimately still has to connect to the bank through a POS terminal or ATM, with the bank’s ledger as the basis.

Then whose accounts determine Bitcoin? Bitcoin does not need a bank, so where is its ledger stored? The answer is: it is stored with every Bitcoin user.

Bitcoin clients come in two kinds: lightweight and full. In every full client, there is stored a record of all transactions since Bitcoin first came into being, and it stays synchronized with the network. A full client that runs continuously and maintains all functions is also called a “node” in the Bitcoin network.

Of course, this master ledger grows larger and larger; it is already close to 120 GB now. Fortunately, not every Bitcoin user needs to keep the full record. The task of preserving transaction records will inevitably rely more and more on professional institutions to maintain it.

The complete transaction record also determines the balance of each account. For example, if you look at your bank statement from the beginning: in some year and month you open the account and deposit 500, in some year and month you spend 300, on some day you remit in another 200, then spend another 100. If the above records cover all transactions, then we can immediately calculate that your “balance” is 500-300+200-100=300 yuan.

So once we know all the transaction records since the creation of Bitcoin, we can calculate how much balance each account has.

Naturally, in order to have the right to initiate a remittance, in addition to controlling the private key, your account must also have sufficient balance.

So, for example, if I control the private key of some address (and this address has sufficient balance) and want to issue a remittance (to another address), as said earlier, it is like signing a remittance slip with a cross-seam seal, specifying how much money is to be sent from the account under my name to another account. But to whom should I hand this remittance slip for settlement? When I swipe a bank card, the transaction is reported to the bank, and the bank is responsible for verification and settlement. But a transaction I issue with a Bitcoin wallet is not handed to any single institution; instead, it is directly “broadcast” to the entire network.

After hearing the broadcast, other Bitcoin users verify two things: first, whether you have the authority to control that address—in other words, whether the “seal” you placed on this transaction is valid; second, whether you have enough balance to complete the payment—that is, they add up all the transactions that have previously occurred at that address and see whether the balance is enough to cover this new expense. If both checks pass, then they will help you continue broadcasting it. In this way, one spreads to ten, ten to a hundred, and valid transactions very quickly spread across the world. In the end, this transaction will be recorded by all Bitcoin users.

So Bitcoin uses a shared public ledger to replace the role of the bank, allowing all Bitcoin users together to take on the roles of verification and settlement.

Of course, there is still another problem here—this process above has a serious loophole, namely that broadcasting from one person to ten to a hundred across the entire network takes time after all. So what if I broadcast two mutually contradictory transactions at the same time?

Just now we said that, in order to determine whether a transaction is valid, two things must be verified: first, whether the private-key signature is valid; second, whether the balance is sufficient. The private-key signature part can never be forged, no matter what, but the balance issue is troublesome.

For example, Liu Bei has a balance of 100 yuan in his account. Liu Bei initiates a remittance, intending to transfer 100 yuan to Guan Yu. He seals the transaction form with a seam-seal stamp, and broadcasts it. Huang Zhong hears this remittance form, checks it, and finds that the signature is valid and the balance is sufficient, so he believes this transaction is valid.

But Liu Bei is very bad. At the same time, he also initiates another remittance, saying he wants to transfer 100 yuan to Zhang Fei. He stamps another seam seal on it and broadcasts that remittance form, but first lets Ma Chao hear it. Ma Chao looks at it and sees that the signature is valid and the balance is sufficient, so he too believes this transaction is valid.

Then Huang Zhong and Ma Chao both continue broadcasting the transactions they believe to be valid, and Zhuge Liang receives these two broadcasts at the same time. Zhuge Liang is then at his wit’s end: he hears Huang Zhong say that Liu Bei has already transferred his 100 yuan to Guan Yu, but he also hears Ma Chao say that Liu Bei’s 100 yuan went to Zhang Fei. If both transactions are valid, then Liu Bei originally had only 100 yuan, and now Guan Yu and Zhang Fei each have an extra 100 yuan. That obviously won’t do, or else if these three kept shuffling money back and forth, wouldn’t they become infinitely rich? So either Guan Yu gets the money or Zhang Fei gets the money; only one of these two transactions can be valid. But which one is valid, exactly? Should we take Huang Zhong’s record as authoritative, or Ma Chao’s?

Solving this problem is the most fundamental technical invention of Bitcoin; this is the key significance of so-called “blockchain” technology. Let me explain below.

4. Anti-counterfeiting: computing-power competition vs. appeal to authority

As mentioned earlier, if a public ledger is to replace the bank, a crucial problem must be solved: preventing the same money from being spent twice, the so-called “double spending.” We must ensure that each sum of money can only be spent once, and that among mutually contradictory transaction records, only one may count as authoritative.

Now Huang Zhong records that Guan Yu gets the money, while Ma Chao records that Zhang Fei gets the money. Should we listen to Huang Zhong or to Ma Chao? Of course, we could also listen to neither, in which case the money is still in Liu Bei’s hands—but that would actually be a third record. Where exactly the money is in the end—whether with Guan Yu, Zhang Fei, or Liu Bei—only one version can ultimately be recognized. So who gets the final say?

Whoever has the higher rank gets listened to? In reality it is probably like that. For example, if a creditor says you owe him money and you say you’ve already paid it back, then if the dispute goes to court, whether money was paid or not is decided by the judge; or take a bank: if the teller says there’s no money left in your card, but you complain to a superior and the superior checks and finds it was a system failure and you actually do have money in your card, then the superior’s judgment still prevails. If you don’t trust the whole bank, you can go further to the court or to the government; in the end, it is always the institution with the greatest power that decides.

But now Bitcoin appeals to a public ledger, where everyone on the network can participate, yet online communication does not require face-to-face contact, nor real-name authentication, and it doesn’t matter how high or low your rank is. In fact, you may not even know how many accounts a person has. For all we know, the Guan Yu and Zhang Fei accounts might both be Liu Bei’s own “aliases,” with him just moving money from his left hand to his right hand.

In such circumstances, we cannot say that the high-ranking person decides, nor can we say that the many decide, because online, rank cannot be seen, and numbers can be fabricated. In short, both traditional democracy and autocracy are unworkable.

Bitcoin’s inventor, Satoshi Nakamoto, came up with a clever idea. In essence, it is still majority rule, but the contest is not based on power or on headcount; instead, it is a contest in “computing power.”

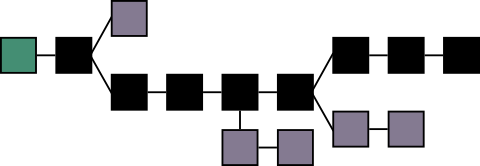

How is this contest carried out? Everyone does a decryption game together. Satoshi Nakamoto designed it so that the record keepers on the Bitcoin network bundle together the transactions they have recorded over a certain period of time, but this aggregation is not a simple listing; it must follow a set of game rules. A batch of transaction records bundled according to those rules is called a “block,” so the Bitcoin “public ledger” linked together by blocks one after another is also called the “blockchain.”

And the rules for bundling transaction records also make use of wondrous “cryptography,” meaning that bundling is very difficult, but once it has succeeded, it is very easy for others to verify in reverse whether the bundle meets the requirements. The transaction record submitted by the first person to successfully bundle it is therefore the most authoritative.

To put it in a metaphor, it is like giving everyone a difficult problem to solve together: whoever solves it first is the best, and everyone listens to that person. Then the next game continues, bundling the next batch of transaction records.

Of course, this kind of problem-solving game can be done together by everyone. The computing power of 10 people added together is equivalent to one person spending 10 times as much time. So a competition in computing power is still really a competition in the strength of each side’s coalition. If I have fifty thousand infantry behind me and you have 830,000 troops behind you, then obviously my side is stronger. But the question is whether I really have that much power behind me, or whether I’m just bragging. In the end, only a problem-solving contest can reveal the truth: whichever side solves faster is stronger.

But what if Huang Zhong solves the answer first, and Ma Chao pretends not to see it (or really doesn’t see it, since broadcasting the answer also takes time), then works furiously for a while and also solves it? What then? Which of these two answers is more trustworthy? Doesn’t the question of whether to listen to Huang Zhong or Ma Chao still remain?

Let me add one thing here: because the answer to the “bundling game” depends on the objects each side needs to bundle (the transaction records), Huang Zhong and Ma Chao are recognizing different transaction records, so their answers are different too. But both can still be “correct answers”; a correct answer means “bundling completed according to the game rules.”

Indeed, the fact that Ma Chao finishes bundling a bit later than Huang Zhong does not prove that his computing ability is necessarily weaker, because there is an element of randomness in the actual competition. We say a top student is better than a poor student, but it may also happen that on a few individual questions, the poor student happens to guess right while the top student calculates for a long time. So how do we judge? There’s no way around it: we just do more problems. If, after the poor student has finished several sets of questions, he still always performs quickly and accurately, then that can only mean he is not a poor student at all.

So what Satoshi Nakamoto designed was to settle things after 6 blocks, that is, after 6 rounds of bundling. Because Huang Zhong and Ma Chao already diverged on the first block they bundled, the followers of Ma Chao must bundle the next block on top of Ma Chao’s first block, while those supporting Huang Zhong must continue bundling on top of Huang Zhong’s first block; the “blockchain” then splits into two competing branches. Satoshi Nakamoto said that after the initial divergence, whichever branch first reaches the sixth block is the winner. So Ma Chao’s record is not rejected at the very moment Huang Zhong finishes bundling; rather, the matter is not settled until the supporters of Huang Zhong have completed six blocks. If reaching six blocks still cannot prove that Huang Zhong’s side has stronger computing power, that is like an illiterate person scribbling randomly and somehow getting a perfect score on the college entrance exam: theoretically it is always possible, but in practice it can be ignored.

Of course, in actual practice, in most cases, when Huang Zhong is the first to produce the first block, the transaction is basically already “safe and sound” once it is confirmed. Ordinary users, in daily use, only need to see that the transaction they sent has been bundled and recorded by others, and they can basically feel at ease.

The difficulty of this “bundling game” is dynamically adjusted, so that for the entire network, each time someone successfully produces a new block, the average time interval is about 10 minutes. If several consecutive blocks are completed very quickly, the difficulty will gradually increase; otherwise it will gradually decrease. So normally, for a transaction to be finally confirmed after 6 blocks takes about an hour, while the first successful bundling takes about 10 minutes.

Are 10 minutes or 1 hour very long? It should be noted that this time is actually equivalent to the time for “checking banknotes,” not the time for “remitting money.” Bitcoin’s “remittance” is actually credited instantly. Whether it is in-person payment or an overseas transfer, as long as you are connected on the internet, the remittance can be completed instantly; it is just that to ensure absolute safety, you need to wait for confirmation.

5. Issuance: Bitcoin mining vs. the central bank

So, after all, did Liu Bei send money to Guan Yu or to Zhang Fei? What do Huang Zhong, Ma Chao, and the others have to do with this matter? What good is it for them to help with recording and bundling? Of course there must be some benefit, in order to keep this system running. On the one hand, when Liu Bei sends money, in addition to the portion received by Guan Yu, it generally needs to include a certain handling fee. Whoever first completes the bundling and includes Liu Bei’s transaction record in it can obtain all the fees attached to these transactions (of course, if a group of people completes the bundling together, they still have to divide the spoils internally). If Liu Bei is especially stingy and does not add even a little fee, then those participating in the bundling competition can simply pretend not to see it and not help him bundle, until someone, in a burst of good will, voluntarily helps record it for free, and only then can the transaction be confirmed. And the more fees are given, the more everyone scrambles to record it. So only those who give enough fees can ensure that the first confirmation arrives in about 10 minutes; if they give too little, there is no guarantee. How much is appropriate depends on the network conditions at that time, and of course some wallet clients will intelligently provide reference suggestions.

Also, in the early days of Bitcoin’s development, there were not many transactions and not much in the way of fees. How, then, could people be incentivized to participate in the bundling competition? Satoshi Nakamoto was again very clever and embedded the “currency issuance” process right here. Satoshi Nakamoto stipulated that the person who successfully bundled a block could, in addition to receiving the fees from all transactions in that block, also receive an extra reward, and this reward Bitcoin was newly created out of thin air. This batch of new coins would also be automatically sent to the address provided by the user who won the bundling game. In the beginning, even if no actual transactions took place, the bundling game still proceeded at a pace of one block every 10 minutes, and these newly issued coin rewards were the original source of Bitcoin.

For roughly the first four years or so (counting one block as 10 minutes; because of Bitcoin’s accelerated development, in actual fact it was a little over three years), each successful bundler could receive a reward of 50 bitcoins. In the second four-year period this was halved to 25; thereafter the reward is halved every four years. The current new-coin reward is 12.5. We know that geometric sequences converge very quickly; in another decade or two, the output of new coins relative to transaction fees may become negligible.

This allows the computing-power competition to incidentally perform the function of a central bank as well, namely, currency issuance. The issuance of modern credit money is in fact a source of wealth polarization. In reality, the closer you are to the source of issuance—financial people, for instance—the easier it is to make money generate money, to earn through multiplication. Those farther from the center can only earn through addition. Moreover, any central bank will always keep issuing more and more money, so currency always becomes more and more depreciated. This is praised as stimulating consumption, and many economic arguments can be made for why money must depreciate. But in the final analysis, it is nothing more than the fact that they hold power, and whether you accept it or not, you have to accept it.

Bitcoin, through this decentralized issuance method, allows anyone with computing power to obtain new coins. Moreover, the increase in the supply of new coins is not decided capriciously by a small number of power holders; rather, from the very beginning, it was fixed as a convergent geometric sequence, ultimately ensuring that over countless years there is a definite upper limit on the total amount of Bitcoin created (21 million).

Of course, people brainwashed by central-bank economics will feel that this model is wrong, and believe that a currency that keeps depreciating is a good currency, while a currency that becomes ever more scarce is very bad. I will not argue this issue here. But in any case, if you hope that the money in your hands will not depreciate, if you hope that currency will always remain scarce, then you can never expect any central bank to issue such a currency; only Bitcoin has realized this dream.

Since new-coin rewards can be obtained from the computing-power competition, Bitcoin’s computing-power competition is also called “mining,” and obtaining new coins is more like panning for gold than relying on a printing press. To participate in mining, you do not need to apply to anyone. You only need to set up the relevant computing equipment anywhere that can connect to the internet, and you can get started.

6. Market: Bitcoin exchange vs. foreign exchange/stock exchange

The above has basically finished explaining the basic principles of Bitcoin. To summarize: owning Bitcoin essentially means owning several “accounts” with balances. These “accounts” are made up of a pair of “private key—public key.” The public key is made known to others, allowing others to remit money into it (or to obtain new coins by participating in mining), while the private key is equivalent to a stamp only you control, used to sign transactions and thereby draw on your own balance to remit money to others. All transactions are recorded by the entire Bitcoin network, forming a “public ledger,” that is, the “blockchain.” How this public ledger keeps accounts is decided by the “computing-power game.” Each time the winner of the computing-power game has the right to bundle a set of transaction records and obtains the fees in that batch of transactions, along with the corresponding new-coin reward. This activity of earning new coins by taking part in the bundling game is called “mining.”

Put simply, maintaining the reliability of the Bitcoin transaction system only requires these two broad kinds of activities: private-key issuance and accounting competition. There is no need for the centralized financial system from the central bank all the way to the bank counter to maintain it.

But of course, as the Bitcoin network develops, many specialized intermediary institutions will also appear, taking on corresponding roles.

For example, on the mining side: in the beginning, computer enthusiasts mined individually on their personal computers, but later, as the computing-power game became more and more difficult and mining increasingly required collective effort, “mining pools” emerged. These are like military camps, concentrating combat power to mine together and then dividing the rewards afterward. Professional mining pools and large-scale mining farms have already become the main force of Bitcoin’s “mining industry.”

Take transactions, for example. Bitcoin transactions do not originally require intermediaries; you do not need to go through a bank in order to transfer money overseas. As long as two people are connected to the internet, they can transact at any time. If I want to get Bitcoin from you, then I just send you my public address and let you transfer Bitcoin into it—that is enough. Of course, the way I then pay you the corresponding RMB or other goods in return, to make an equivalent exchange, is something for us two to negotiate freely. If I want to spend the Bitcoin balance I have, then likewise I only need to find another person who wants to acquire Bitcoin, agree with him on how to exchange it, and you pay the coins while he delivers the goods. A more advanced use is to have multiple private keys manage one account and carry out “multi-signature”; I won’t go into that here.

Bitcoin transactions do not require intermediaries, but that does not mean intermediaries cannot exist. Intermediaries are a role that the free market will inevitably give rise to, and the Bitcoin market is no exception. For example, when it comes to exchanging Bitcoin for renminbi, of course we can always contact one another privately and complete the exchange. But once enough people have such a need, and everyone wants to complete transactions at a faster speed and at a more reasonable price, then there is room for intermediaries. Exchanges that provide continuous auction trading will naturally emerge as well. An exchange first helps customers deposit renminbi and Bitcoin, customers submit their bids to the exchange, and then the exchange automatically matches customers whose quotes fit together and completes the transaction between them. The latest matched transaction quote on the exchange then forms the “market price.” This price can serve as a reference for other private transactions, but it is by no means decisive. If you have the ability, you could even sell 1 Bitcoin for 1 million outside the exchange right now—as long as someone is willing to buy it.

That is the principle of an exchange. In fact, it has nothing to do with Bitcoin; other foreign-exchange exchanges, stock exchanges, and the like all work on similar principles. I still mention it because too many people have misunderstandings, thinking that Bitcoin is some kind of thing that exists inside an exchange, rather than something that you can fully control yourself outside of any exchange. This is probably due to the illusion created by popular stock exchanges, because we ordinary people generally cannot “withdraw” stock from a stock exchange, nor can we privately trade stocks outside the exchange. But this is not really a characteristic of stocks themselves; it is a set of rules established by the government in order to regulate you, and by the big players in order to harvest you. In any case, an exchange at most provides custodial and deposit functions; Bitcoin transactions themselves have never depended on the existence of exchanges.

Because Bitcoin exchanges originally arose spontaneously in the free market, rather than being set up top-down by governments or financiers, they already bore the mark of freedom from the very beginning. For example, common foreign-exchange exchanges or stock exchanges are not open 24 hours a day, and some even have rules such as you can only sell the day after you buy. Features of Bitcoin exchanges such as crossing national borders, operating around the clock, and having no limit-up or limit-down restrictions are striking, but in fact they are perfectly natural. By contrast, the various constraints of traditional exchanges actually make little sense.

Finally, here is a comment I recently posted about the issue of forks:

Some people are making such a fuss that it sounds as if a fork were the end of Bitcoin. Maybe what they care about is only whether next month’s futures contracts will blow up, but if we look at long-term development, a fork is not that frightening; it is even a good thing.There is also alarmism about the so-called “replay attack” after Bitcoin forks. I saw people saying that, in order to avoid it, one should first keep coins on an exchange rather than in one’s own wallet. Anyone who makes such a suggestion is either utterly foolish or has some hidden agenda. At any time, a cold wallet whose private keys you control yourself is always the safest way to store Bitcoin, without exception and without a second-best.

A so-called replay attack is nothing more than the fact that the two branches after a fork share the same private keys, public keys, and transaction format. If you control the private key of address A on fork 1, that means you also own address A on fork 2. A transaction sent from address A to address B may be recognized on both forks at the same time. If you only want to send from A to B on fork 1, but a troublemaker on the network can “help” you send from A to B on fork 2 as well, that is a replay attack.

So it is very simple to avoid replay attacks: while you initiate A-to-B on 1, initiate A-to-C on 2, making sure that the three addresses A, B, and C are all private keys you control. If both transactions succeed, then your coins have successfully forked, and you no longer need to fear replay attacks. If you are replay-attacked, that is also fine: both transactions were sent to B, but B still belongs to you, so just try again. As long as you control the private keys yourself, the coins can never be lost.

Of course, if you hope to sell your coins immediately after the fork, then you probably still need to keep them on an exchange in advance. But if your concern is only the safety of holding them yourself, then controlling your own private keys is always the safest, with no exceptions.

Translated from the Chinese original with AI assistance. The original text is authoritative.

Leave a Reply